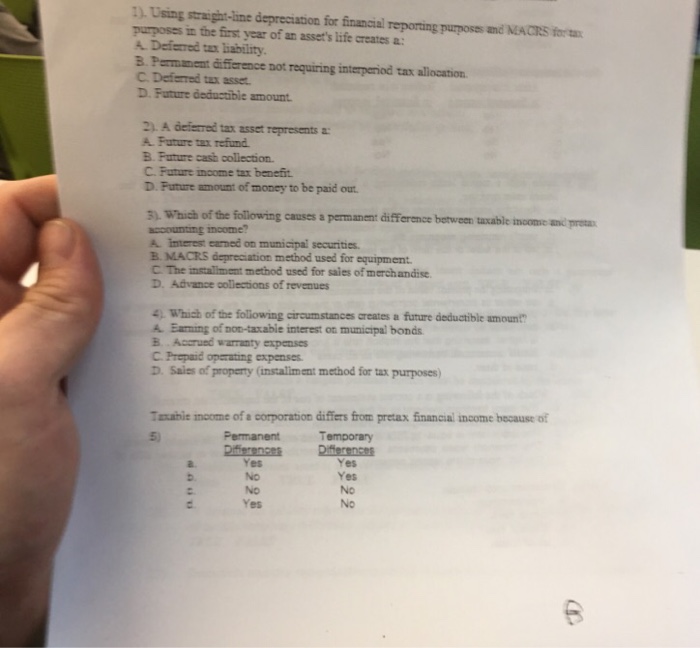

Which of the Following Circumstances Creates a Future Taxable Amount

Accrued compensation costs for future payments. Sams Year 2 taxable income was 175000 with a corresponding tax liability of 30000.

Solved Using Straight Line Depreciation For Financial Chegg Com

Earning of non-taxable interest on municipal bonds.

. Yes Yes 33 15. Service fees collected in advance from customers. The taxpayer might obtain a refund or credit upon amending past tax returns to apply the proposed regulations.

Answer d is a permanent difference that. When PPP loan forgiveness is granted. This may happen if a company uses the cash method for tax preparation.

A deferred tax asset is an item on a companys balance sheet that reduces its taxable income in the future. In order to avoid a penalty for underpayment of estimated tax what is the minimum amount of Year 3 estimated tax payments that Sam can make 30000 33000 45000 50000. Such a line item asset can be found when a business overpays its taxes.

Specifically IRM 25261 outlines responsibilities of the TS group that is designated to make all of the CR assessments. Sales of property installment method for tax purposes. If you dont receive your Form 1099-G by mid-February you may call.

Service fees collected in advance from customers. For Year 3 Sam expects taxable income of 250000 and a tax liability of 50000. Which of the following circumstances creates a future deductible amount.

If there are no tax consequences from repayment of. Deferred tax liabilities are the amounts of income taxes payable in future periods in respect of taxable temporary differences. A deferred tax liability is a listing on a companys balance sheet that records taxes that are owed but are not due to be paid until a future date.

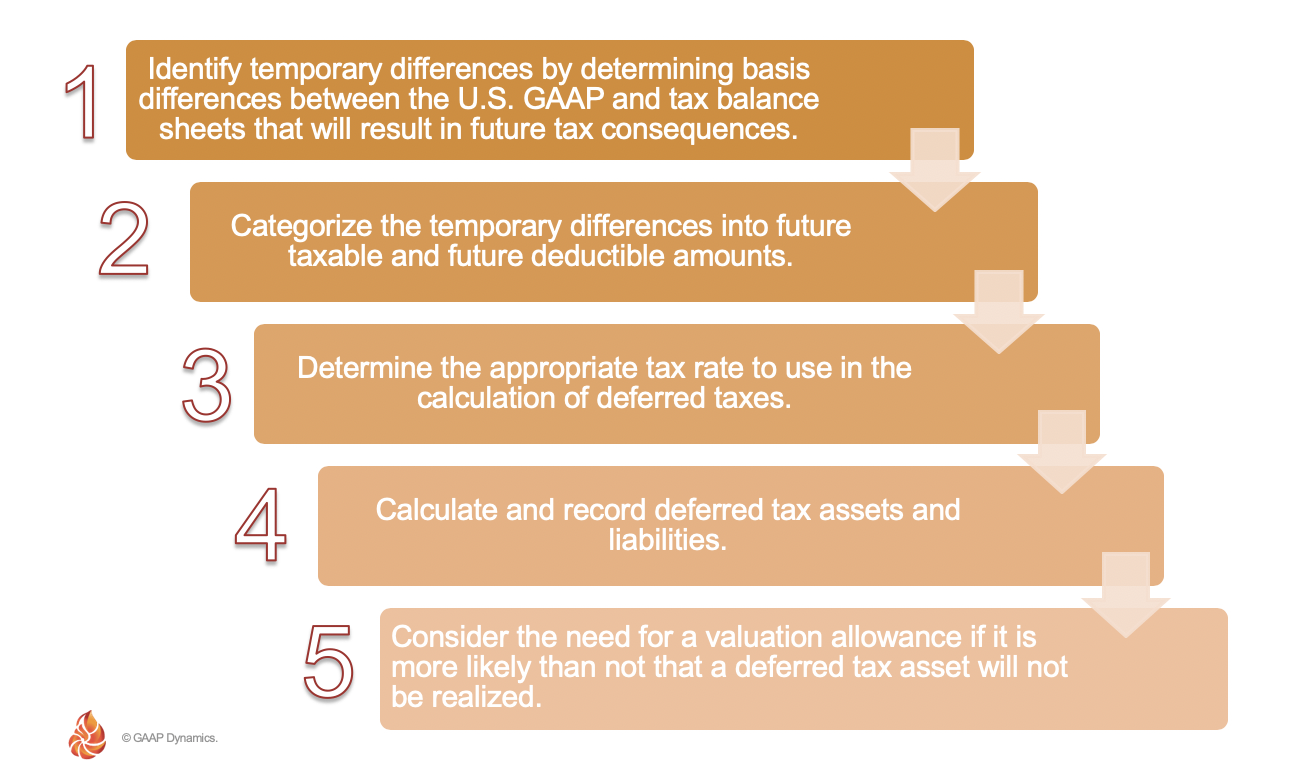

Future Future Taxable Amounts Deductible Amounts a. Accrued compensation costs for future payments. Paragraph IAS 1235 specifically emphasises that the existence of unused tax losses is strong evidence that future taxable profit may not be available and that an entity with a history of recent losses recognises a deferred tax asset arising from unused tax losses or tax credits only to the extent that the entity has sufficient taxable temporary differences or there is.

This would result in what type. Which of the following circumstances created a future taxable amount. Straight-line depreciation for financial reporting and accelerated depreciation for tax reporting.

Straight-line depreciation for financial reporting and accelerated depreciation for tax reporting. Taxable when received recognized for. Which of the following circumstances creates a future taxable amount.

Taxable when received recognized for financial reporting when earned. Taxable when received recognized for financial reporting when earned. Deferred tax assets are the amounts of income taxes recoverable in future periods in respect of deductible temporary differences carry forward of unused tax losses and carry forward of unused tax credits.

2021-48 provides that taxpayers may treat amounts that are excluded from gross in connection with the forgiveness of PPP loans that are received or accrued. Answers a and b are temporary differences that would result in future. Accounting depreciation meaning future taxable income.

Straight-line depreciation for financial reporting and accelerated depreciation for tax reporting. Interest received on municipal bonds. This IRM section describes the procedures for criminal restitution CR and restitution-based assessments RBA made by Technical Services TS.

The Michigan Unemployment Insurance Agency UIA administers the unemployment insurance program that provides temporary financial assistance to individuals who become unemployed through no fault of their own. Taxable when received recognized for. Program Scope Objective.

Remember that the accounting goals under SFAS 109 was to not only record the amount of taxes payable for the current year but to establish assets and liabilities for the future tax consequences of events recognised in the current year financial statements or tax return. Accrued compensation costs for future payments. As eligible expenses are paid or incurred.

Which of the following circumstances creates a future taxable amount. Which of the following circumstances creates a future taxable amount. Conversely if the revenue is recognised for tax purposes when the goods or services are received the tax base will be equal its carrying amount.

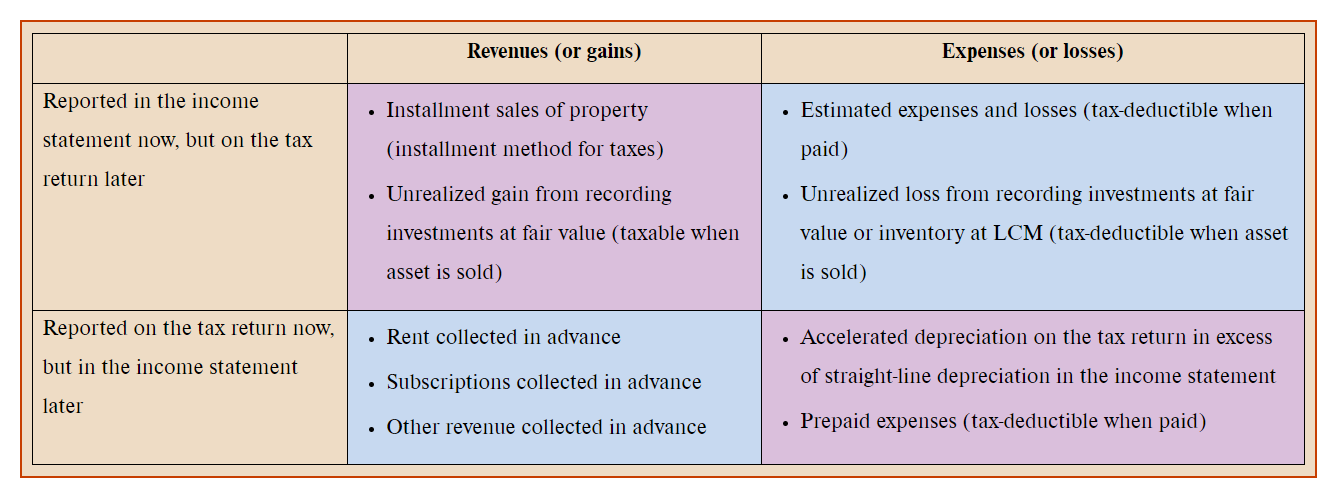

Taxable when received recognized for financial reporting when earned. In particular a taxpayer in either of the following circumstances might benefit from taking action sooner than later. One results in a future taxable amount such as revenue earned for financial accounting purposes but deferred for tax accounting purposes.

It is important to distinguish between the temporary and permanent differences. Multiple Choice Service fees collected in advance from customers. If the revenue is taxed on receipt but deferred for accounting purposes the tax base of the liability is equal to equal to nil as there are no future taxable amounts.

Will exceed future financial accounting income. The ED rules have already applied to a dividend such that the taxpayer has included marginal amounts in taxable income. To the extent such tax-exempt income.

Taxable when received recognized for financial reporting when earned. Which of the following creates a permanent difference between financial income and taxable income. A company uses the equity method to account for an investment.

This money will. Service fees collected in advance from customers. Service fees collected in advance from customers.

Accrued compensation costs bonuses paid in the future. Straight-line depreciation for financial reporting and accelerated depreciation for tax reporting. Benefits are paid through taxes on employers covered under the Michigan Employment Security Act.

When an application for PPP loan forgiveness is filed or. Which of the following circumstances creates a future taxable amount. Which of the following circumstances creates a future taxable amount.

In order to determine taxable income each January the EDD sends a Form 1099-G to each individual for the total unemployment insurance benefits paid during the prior year. In future years tax depreciation will be less than financial. The second type of temporary difference is a future deductible amount.

Service fees collected in advance from customers. Straight-line depreciation for financial reporting and accelerated depreciation for tax reporting Which of the following usually results in an increase in a deferred tax liability. Which of the following circumstances creates a future taxable amount.

2

What Are Deferred Tax Assets And Deferred Tax Liabilities Article

Ch19 Kieso Intermediate Accounting Solution Manual

Chapter 16 Flashcards Chegg Com

Ch19 Kieso Intermediate Accounting Solution Manual

Ch19 Kieso Intermediate Accounting Solution Manual

Ch19 Kieso Intermediate Accounting Solution Manual

Ch19 Kieso Intermediate Accounting Solution Manual

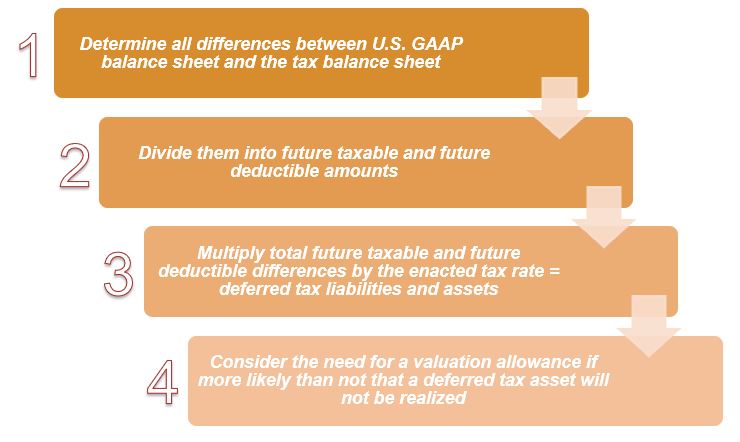

Accounting For Income Taxes Under Asc 740 Deferred Taxes Gaap Dynamics

Income Taxes Gaap Dynamics

Valuation Allowance For Deferred Tax Assets A Quick Guide

Ch19 Kieso Intermediate Accounting Solution Manual

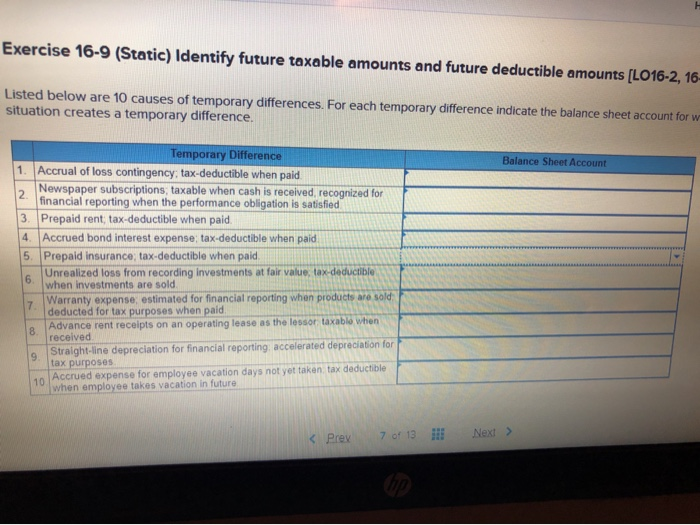

Solved Exercise 16 9 Static Identify Future Taxable Chegg Com

Ch19 Kieso Intermediate Accounting Solution Manual

2

2

296075494 Liabilities Toa

Income Taxes Gaap Dynamics

2

Comments

Post a Comment